Accounting Matt Valentine•April 27, 2026

Matt Valentine•April 27, 2026

Trust Accounting for Property Managers: A Complete Guide (2026)

Matt Valentine•April 27, 2026 Matt Valentine•April 27, 2026

Matt Valentine•April 27, 2026

Every dollar of rent you collect on behalf of an owner isn’t your money.

Every security deposit a tenant hands over isn’t your money either.

You’re holding those funds in trust. That’s not a metaphor. It’s a legal obligation with real consequences if you get it wrong.

Commingling trust funds with your operating account is illegal in every state. The penalties range from fines to license suspension to criminal charges, depending on severity and jurisdiction.

This guide covers how trust accounts work, how to set one up, how to reconcile properly, and the mistakes that get property managers into trouble.

A trust account is a dedicated bank account used solely to hold funds that belong to other people. In property management, those “other people” are your clients: property owners and their tenants.

You are the trustee. The owners and tenants are the beneficiaries. The money belongs to them, not to you.

| Fund Type | Example | Who It Belongs To |

|---|---|---|

| Rent payments | Monthly rent collected from tenants | Property owner |

| Security deposits | Move-in deposits from tenants | Tenant (until applied or returned) |

| Advance rent | Last month’s rent, prepaid rent | Tenant/owner |

| Maintenance reserves | Funds held for future repairs | Property owner |

| HOA assessments | Collected on behalf of an association | The association |

The only exception most states allow: a small amount of your own funds (typically $100-$200) to cover bank service charges.

Trust accounting isn’t just a best practice. It’s a legal requirement and one of the most common areas where property managers face compliance issues.

Here’s why it matters.

In most states, property managers operating under a real estate broker’s license are legally required to maintain trust accounts. State real estate commissions in California, North Carolina, and Florida have all flagged trust fund handling as a primary enforcement priority.

If your business gets sued, faces a tax lien, or goes through financial difficulty, funds in a properly structured trust account are protected from your creditors. If those same funds were in your operating account, they’d be at risk.

Trust fund violations are a top reason state commissions audit, fine, suspend, or revoke property management licenses. One commingling violation can end a career.

Owners want to know their rental income is being handled professionally. Clean trust accounting with regular statements builds the kind of confidence that keeps clients renewing.

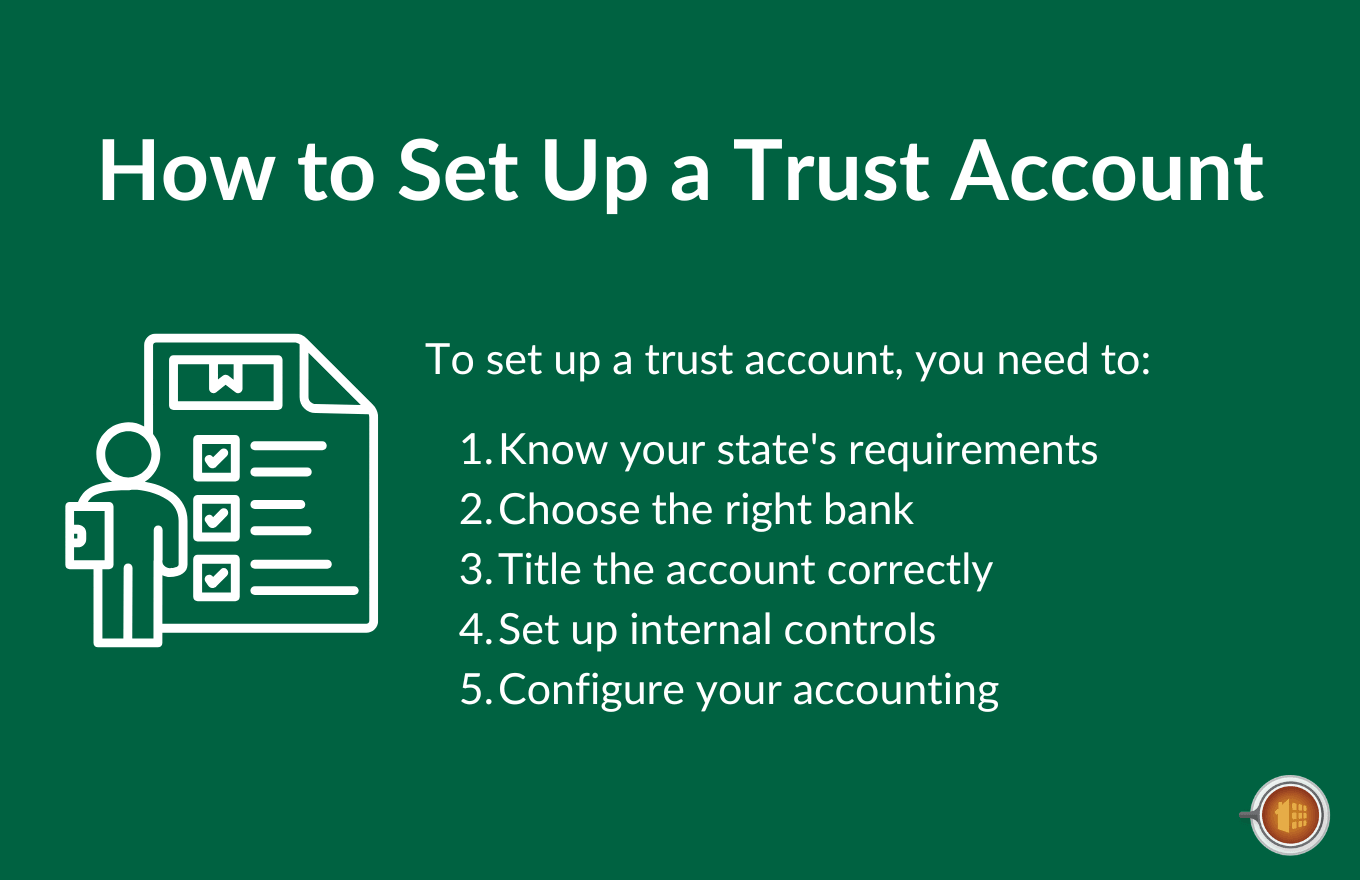

Setting up a trust account correctly from the start prevents most compliance issues down the road. There are specific steps to follow, and the details matter.

Let’s walk through each one.

Before opening any account, research your state’s trust accounting laws. The specifics vary significantly.

Key questions to answer:

Your state real estate commission’s website is the authoritative source.

Not every bank understands property management trust accounts. Some confuse them with family trusts, estate trusts, or IOLTA accounts.

When choosing a bank, confirm that:

A properly structured trust account provides FDIC insurance of up to $250,000 per beneficiary, not per account. That’s a critical distinction for management companies holding significant funds.

The account name matters for compliance and FDIC coverage.

Example: “Smith Property Management, LLC – Trust Account”

A regular checking account with “trust” in the memo field offers zero legal protection.

Trust account access should be restricted and monitored.

Your software needs to track trust funds separately from operating funds, with individual ledgers for each property owner and tenant.

Every dollar in the trust account should be traceable to a specific client. If you’re holding $340,000 across 200 units, your subsidiary ledgers for all clients combined must equal your bank balance.

If they don’t match, you have a compliance issue.

Monthly reconciliation is the single most important discipline in trust accounting. Most states require it. All states expect it if you get audited.

Here’s what “three-way” means.

| Source | What It Represents |

|---|---|

| Bank balance | Adjusted bank statement balance (accounting for outstanding checks and deposits in transit) |

| Book balance | Your general ledger’s trust account balance |

| Client ledger total | The sum of all individual owner and tenant sub-ledgers |

All three must match exactly. If they don’t, something is wrong.

Pull your bank statement at the end of each month. Compare every transaction to your internal records. Account for outstanding checks and deposits in transit.

Verify that your general ledger trust balance matches the adjusted bank balance. Then add up all individual client ledgers and verify the total matches both.

If your numbers don’t balance, investigate immediately. A discrepancy that sits unresolved for months becomes exponentially harder to fix.

These are the errors that trigger audits, fines, and license actions. Most are easy to avoid once you know what to watch for.

Here are the ones that come up most often.

This is the violation that ends careers. Commingling happens whenever client money mixes with your business money. Common examples:

Having said that, the rules can be nuanced. Some states allow mixed funds temporarily when it’s not practical to separate them (for example, a rent check that includes both the owner’s portion and your management fee). But the expectation is that you separate them promptly.

If an individual owner’s ledger goes negative, you’ve effectively used another client’s funds to cover the shortfall. That’s commingling.

Your software should alert you before this happens. Never allow a disbursement that would create a negative balance.

Skipping reconciliation is how small errors become big problems. A $50 discrepancy in March becomes a $2,000 mystery by December. By then, the audit trail is cold.

Calling your regular business account a “trust account” doesn’t make it one. The bank must set it up as a fiduciary account with the correct legal structure.

Standard FDIC insurance covers $250,000 per depositor, per bank. But a properly structured trust account can be insured up to $250,000 per beneficiary.

If you’re holding $1 million across 10 owners, each owner’s $100,000 is individually insured. If the account wasn’t structured correctly, you might only be covered for $250,000 total.

Most states require client funds to be deposited within one to three business days of receipt. Late deposits are one of the easiest violations for auditors to spot.

Online payment processing that deposits directly into your trust account eliminates this risk entirely.

Managing trust accounts manually (whether in spreadsheets or a general accounting tool) creates the exact conditions that lead to compliance violations. Manual data entry errors. Missed reconciliations. Unclear audit trails. Client funds that can’t be traced.

Mocha Manage was built by CPAs who understand trust accounting at a compliance level.

With Mocha, you can set up trust accounts separate from operating accounts for every owner with individual ledgers in seconds:

Keep internal accounts separate and easily organized while seamlessly following trust account best practices:

Absolutely everything you need to manage your trust accounts, including:

Mocha’s true integrated accounting also prevents negative ledger balances (alerts, blocks, or warnings), protecting you while you focus on what matters most.

Trust funds are tracked separately from your operating money from the moment they enter the system. Every dollar is tied to a specific owner or tenant.

Individual client ledgers reconcile against the trust account balance automatically. And the financial reports your auditor or state commission expects are built into the platform.

For property managers who’ve spent hours on manual reconciliation (or discovered a discrepancy during an audit), the difference between a general accounting tool and a platform built for trust accounting is the difference between hoping you’re compliant and knowing you are.

Try Mocha Manage free to see what trust accounting looks like when it’s built by CPAs who understand the compliance requirements.

What is a trust account in property management?

A trust account holds funds belonging to property owners and tenants, including rent, security deposits, and reserves. Property managers must keep these funds separate from their business operating money.

What happens if I commingle trust funds?

Commingling is illegal in all states. Consequences range from fines and audits to license suspension, revocation, or criminal charges depending on severity.

How often do I need to reconcile my trust account?

Monthly. Match your bank balance, book balance, and client ledger totals. All three numbers must match exactly.

Do I need separate trust accounts for security deposits?

Depends on your state. Some require separate accounts. Others allow a single trust account with clear internal records. Check your state real estate commission.

What’s the deposit deadline for client funds?

Most states require one to three business days from receipt. The exact timeline varies. Late deposits are a common violation.

Can I earn interest on a trust account?

Some states allow it, others require it above certain thresholds. In most cases, interest belongs to the client, not the property manager.

Disclosure: Mocha Manage publishes this blog. This guide is for informational purposes only and does not constitute legal or accounting advice. Trust accounting laws vary by state. Consult an attorney or CPA for advice specific to your situation.