Accounting Matt Valentine•February 9, 2026

Matt Valentine•February 9, 2026

HOA Accounting 101: A Complete Guide for Board Members

Matt Valentine•February 9, 2026 Matt Valentine•February 9, 2026

Matt Valentine•February 9, 2026Managing an HOA’s finances is a big job.

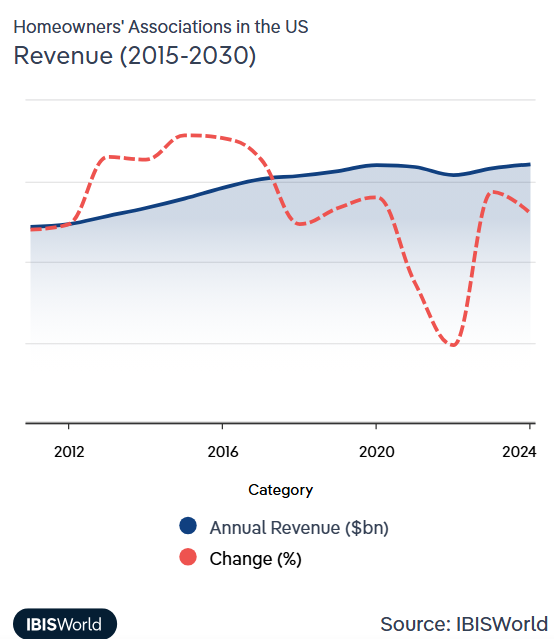

The job only gets bigger, too, with HOA boards managing more funds on average than ever before, according to a study by IBIS World:

With that said, it’s also a job that’s easy to get wrong, potentially leading to legal repercussions and a whole lot of trouble.

Despite this, board members are often not certified accountants. Maybe that’s you.

The good news: HOA accounting follows clear principles that anyone can learn.

The bad news: mistakes can lead to budget shortfalls, compliance violations, special assessments, and angry homeowners questioning where their dues went.

So, let’s jump in together and make sure you have the tools you need to get this right.

The guide below walks you through everything you need to know about HOA accounting, from basic concepts to advanced best practices.

Whether you’re a new board member trying to understand your treasurer’s reports or an experienced president looking to improve your association’s financial management, you’ll find actionable guidance here.

HOA accounting isn’t the same as managing your personal finances or running a small business.

Homeowners associations operate under unique rules that combine non-profit accounting principles with real estate management requirements.

Here’s what makes HOA accounting distinct:

The first decision your HOA needs to make is which accounting method to use.

This choice affects how you record income and expenses, what your financial statements show, and whether you’re following Generally Accepted Accounting Principles (GAAP).

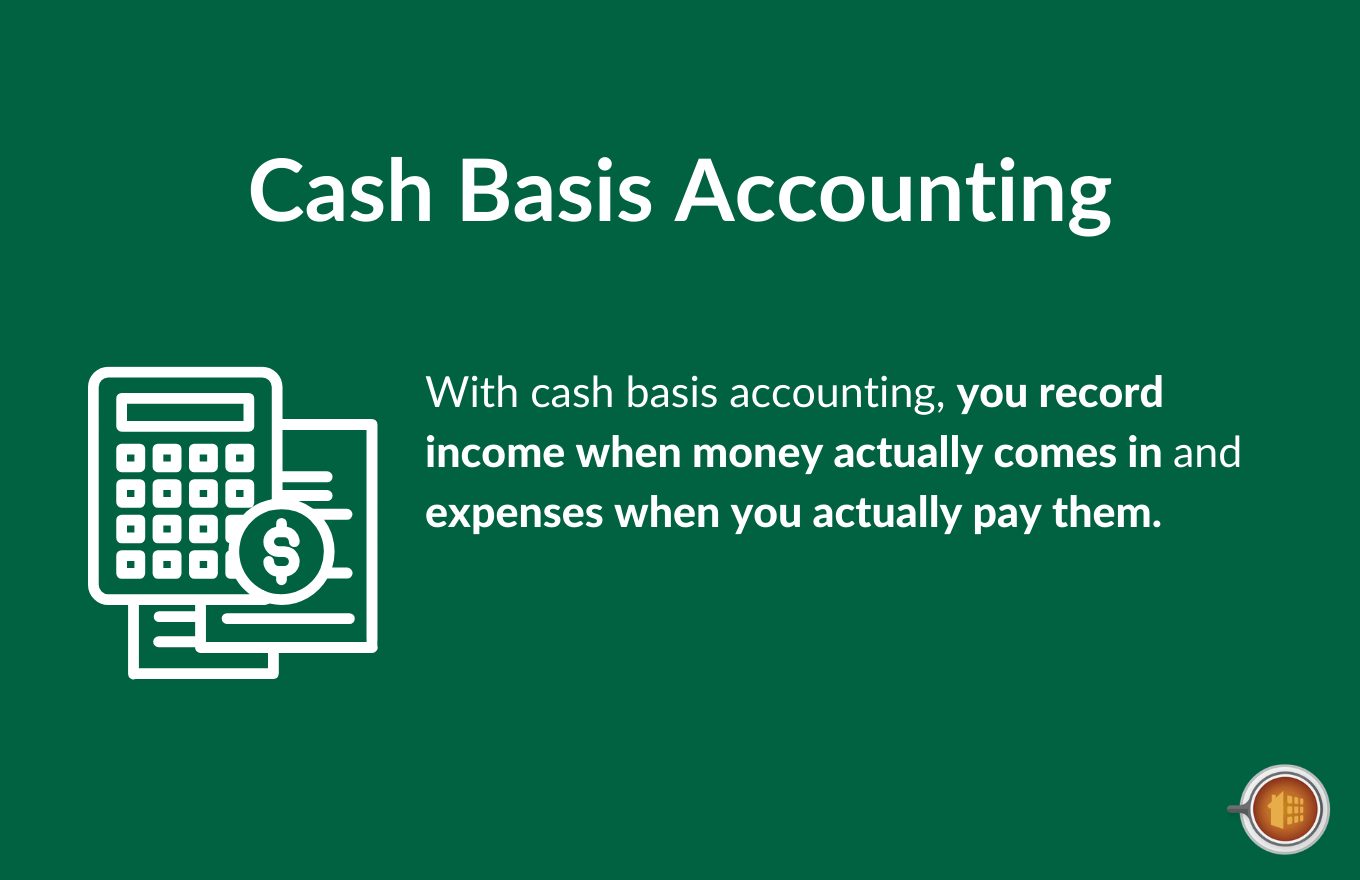

With cash basis accounting, you record income when money actually comes in and expenses when you actually pay them.

If homeowner dues are technically owed in January but the payment arrives in February, you record it in February. If you receive an invoice in December but don’t pay until January, it shows up in January.

Very small HOAs with simple finances and minimal reserve requirements.

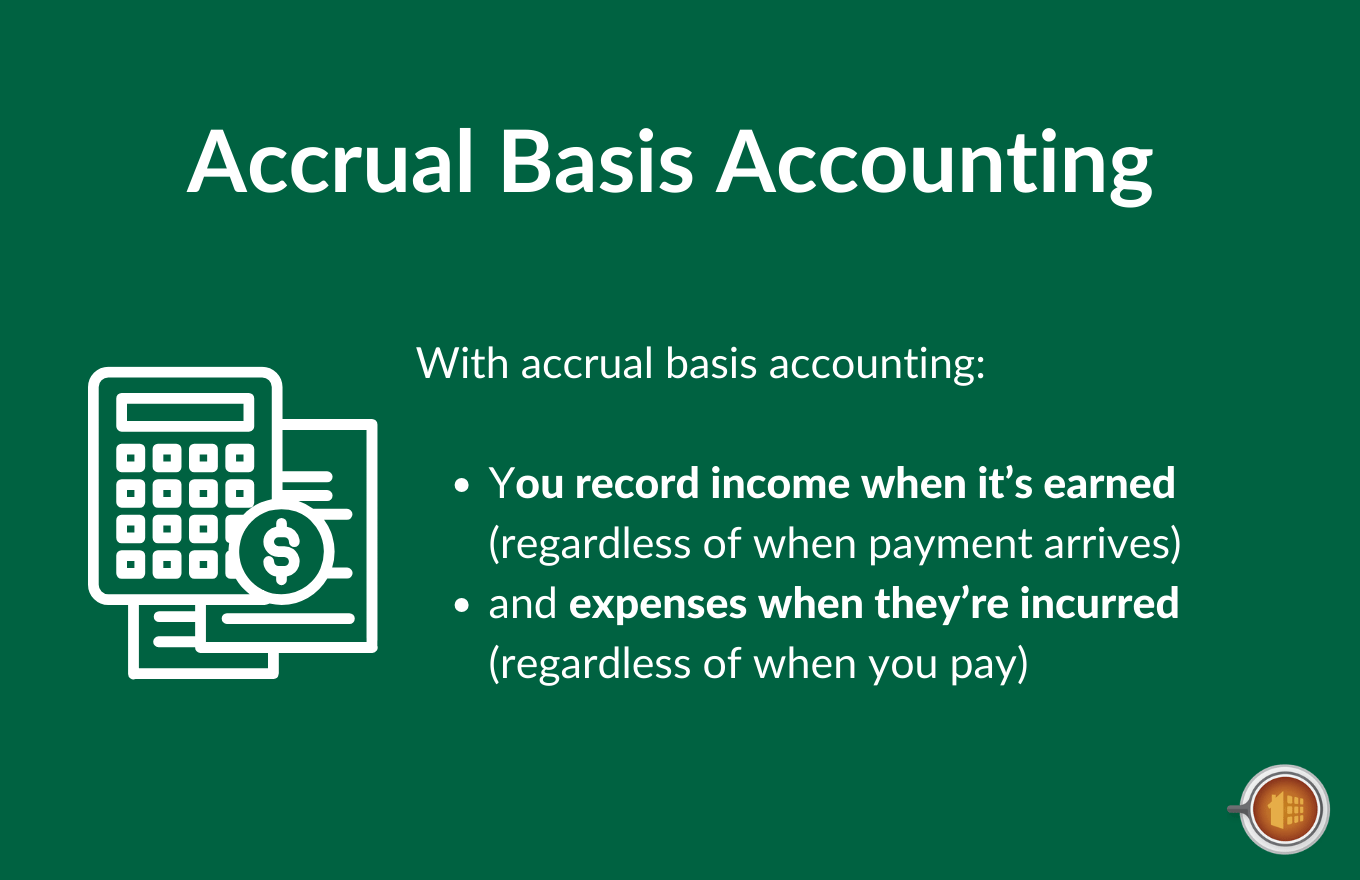

With accrual basis accounting, you record income when it’s earned (regardless of when payment arrives) and expenses when they’re incurred (regardless of when you pay).

If homeowner dues are assessed in January, they show up as income in January even if payments trickle in over the next few months. If a contractor completes work in December, the expense appears in December even if you don’t pay the invoice until January.

Medium to large HOAs, associations with significant reserve funds, and those required by state law to use GAAP.

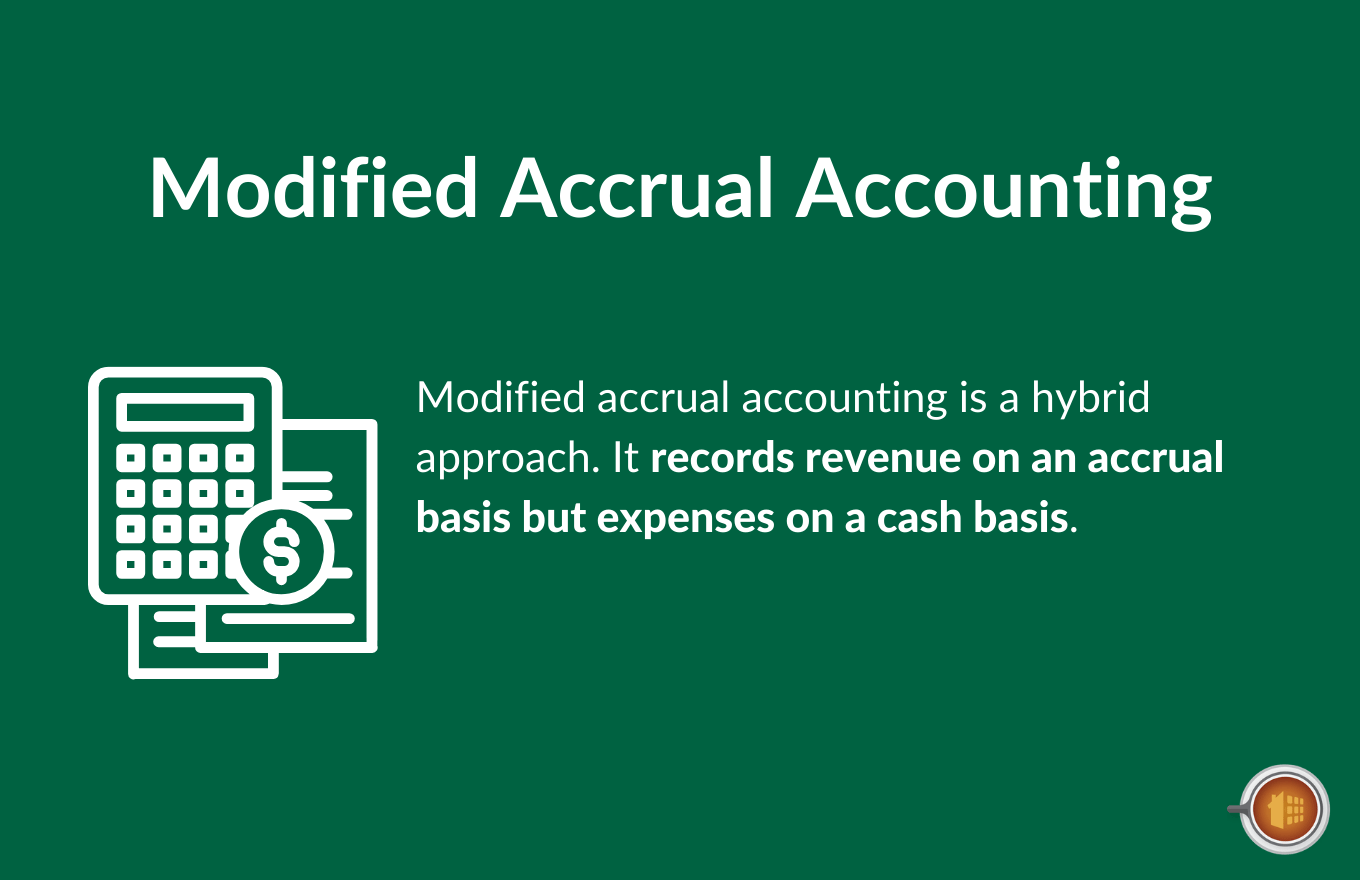

Modified accrual accounting is a hybrid approach that records revenue on an accrual basis but expenses on a cash basis.

You recognize assessment income when it’s billed to homeowners (accrual), but you only record expenses when you actually pay them (cash).

Medium-sized HOAs that want better financial visibility than cash basis but aren’t ready for full accrual accounting.

Most accounting experts recommend accrual basis accounting for HOAs. It provides the most accurate financial picture and is considered the proper method under GAAP.

However, if your HOA is very small (under 20 units), has simple finances, and no state regulations requiring GAAP, cash basis or modified accrual can work.

Check your state’s requirements and your association’s governing documents. Some bylaws specify which accounting method must be used.

Your HOA should produce four core financial statements on a regular basis—typically monthly or quarterly for board review, and annually for all homeowners.

The balance sheet is a snapshot of your HOA’s financial position at a specific moment in time.

It shows what the association owns (assets), what it owes (liabilities), and what’s left over (fund balance or equity).

Fund balance is the difference between assets and liabilities. For HOAs, this is typically separated into operating fund balance and reserve fund balance.

A healthy HOA balance sheet shows adequate cash reserves, minimal accounts receivable (most homeowners are current), and a strong reserve fund balance relative to future capital needs.

The income statement shows all income and expenses over a specific time period—usually a month, quarter, or year.

Unlike the balance sheet (which is a snapshot), the income statement shows financial activity over time.

For HOAs, the income statement should separate operating fund activity from reserve fund activity. You want to see operating income and operating expenses separately from reserve contributions and capital expenditures.

A healthy income statement shows income meeting or exceeding expenses (you’re not operating at a loss) and reserve contributions happening as planned.

The cash flow statement tracks the actual movement of money in and out of your HOA’s bank accounts.

Even if your HOA is profitable on paper (income statement shows more income than expenses), you could still have cash flow problems if homeowners are slow to pay or if you have large expenses concentrated in certain months.

The cash flow statement reconciles your income statement with your actual bank account balance changes.

It typically breaks down into three categories:

Cash from assessments and payments to vendors

Purchases or sales of investments, major capital improvements

Loan proceeds or repayments

This statement helps your board understand whether the association can pay its bills on time and identifies months when cash might be tight.

The general ledger is the detailed transaction record behind all your other financial statements.

Every check written, every assessment collected, every expense categorized—it’s all recorded in the general ledger.

Think of the general ledger as your complete financial history. The other statements (balance sheet, income statement, cash flow) are summaries derived from this detailed record.

Board members don’t typically review the general ledger line by line every month, but it should be available for review when questions arise about specific transactions.

Your chart of accounts is the framework that organizes all your financial transactions.

It’s a list of all the categories (accounts) where income and expenses get recorded. Every transaction gets assigned to one of these accounts.

A well-organized chart of accounts makes it easy to track where money is coming from and going to.

Most HOAs organize accounts into these major categories:

The key is to be specific enough to track meaningful categories but not so detailed that you have dozens of accounts with minimal activity.

Let’s finish by covering a few common mistakes made when it comes to setting up your chart of accounts.

Some of these are basic, but they’re all vital to get right, so they’re worth mentioning:

Don’t have a single account called “Repairs.” Break it down: Pool Repairs, Building Repairs, Landscape Repairs. This makes it easier to identify trends and budget accurately.

Regular ongoing maintenance (pool cleaning, lawn care) goes in operating expenses. Major repairs and replacements go in reserve expenses. Keep them separate.

Don’t lump all income into “Assessments.” Separate regular assessments, special assessments, late fees, and other income sources so you can see exactly where money is coming from.

Homeowner assessments are the lifeblood of your HOA’s finances.

Most of your income comes from these regular dues, so collecting them efficiently and handling delinquencies properly is critical.

Your annual budget determines how much you need to collect in assessments.

Here’s the basic formula:

Total annual operating expenses + Reserve contributions = Total assessment income needed

Divide that total by the number of units and the number of assessment periods (monthly, quarterly, etc.) to get the per-unit assessment amount.

Example:

Most HOAs need to increase assessments periodically to keep pace with rising costs.

Check your governing documents and state law for restrictions on assessment increases. Some states limit how much you can raise assessments without homeowner approval (typically 5-20% per year).

When raising assessments, communicate clearly with homeowners:

Make it easy for homeowners to pay by offering multiple payment methods:

The easier you make it to pay, the better your collection rate will be.

When homeowners don’t pay on time, you need a consistent collection process:

Send a friendly reminder notice. Sometimes homeowners simply forget.

Send a more formal notice indicating the account is past due. Include any late fees or interest charges per your governing documents.

Send a final notice before legal action. Make it clear what will happen next if payment isn’t received.

Turn the account over to your HOA attorney for collection. This may include filing a lien against the property.

Apply your collection policy consistently. Don’t make exceptions for some homeowners but not others—that creates legal liability and resentment in the community.

Your accounting system should clearly show which homeowners are current and which are behind.

Run an aged receivables report monthly to see:

Don’t let receivables pile up. The longer an account goes unpaid, the harder it is to collect.

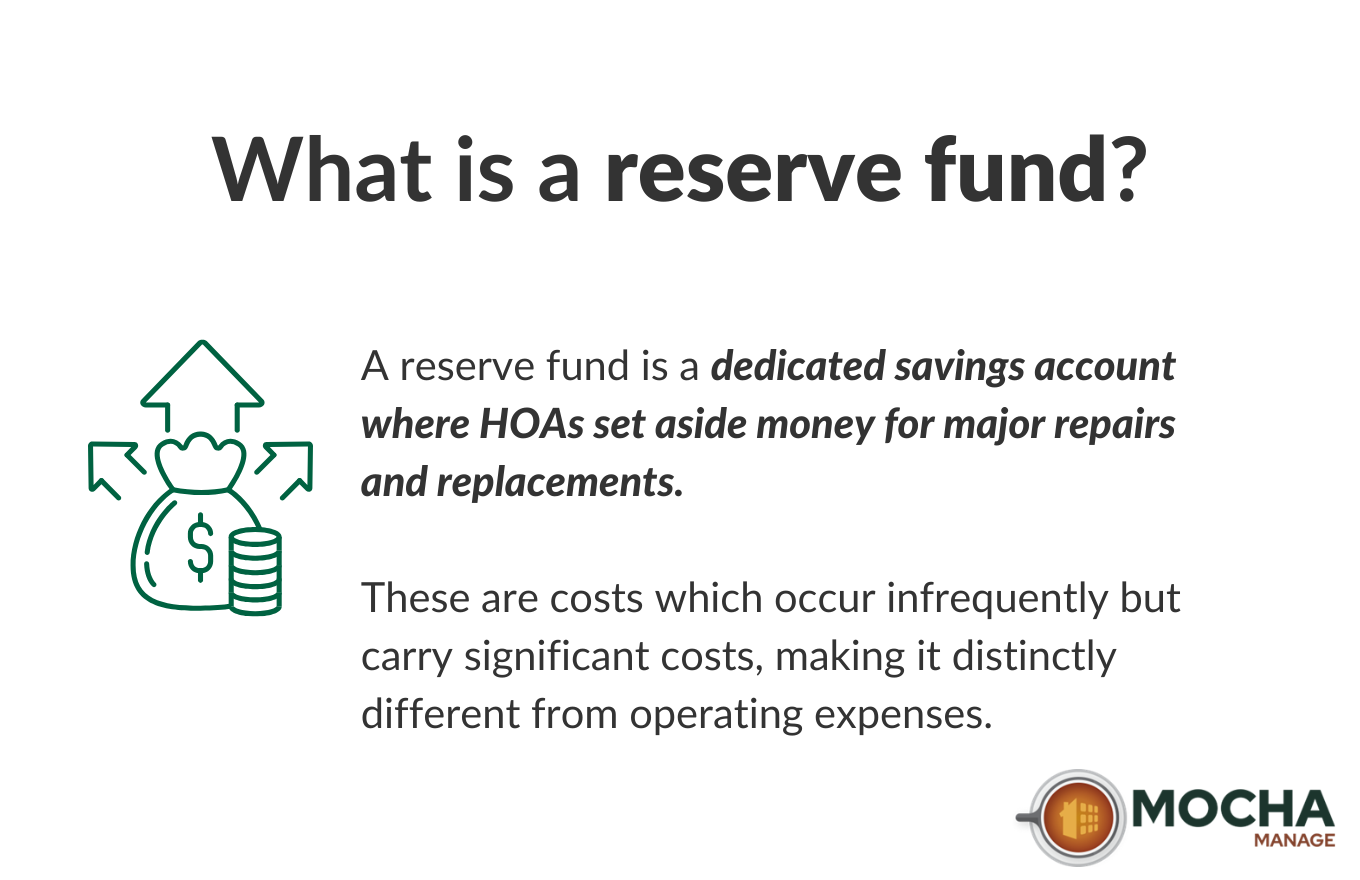

Reserve funds are the HOA equivalent of a savings account—money set aside today to pay for major repairs and replacements tomorrow.

Proper reserve fund accounting is critical to your association’s long-term financial health and property values.

Reserve funds are savings designated for major capital expenditures—repairs and replacements with useful lives longer than one year.

Think of the difference between changing a light bulb (operating expense) and replacing the entire lighting system (reserve expense).

The key distinction: operating expenses are routine and predictable (landscaping, utilities, insurance). Reserve expenses are major, infrequent, and significant.

A reserve study is a professional analysis that tells you:

Most experts recommend updating your reserve study every 3-5 years, with annual reviews to adjust for inflation and changing conditions.

Without a reserve study, you’re guessing. With one, you’re planning.

The ideal reserve contribution amount comes from your reserve study.

The study calculates how much you need to save each year to build adequate reserves without running a deficit.

Most HOAs aim for 70-100% funded reserves, meaning if all major components needed replacement today, you’d have 70-100% of the money required.

If your reserve study shows you need $50,000 per year to adequately fund reserves based on projected future expenses, then $50,000 should be included in your annual budget and allocated to the reserve fund.

This might mean each homeowner pays $40/month in regular assessments plus $15/month for reserve contributions.

Reserve funds must be tracked separately from operating funds.

Your accounting system should clearly show:

When you spend money from reserves for a major project, it should be recorded as a reserve expense, not an operating expense.

Some HOAs face cash flow crunches and consider “borrowing” from reserves to cover operating shortfalls.

This is almost always a bad idea and may be prohibited by your governing documents or state law.

Reserve funds exist for a specific purpose. Using them for operating expenses means you won’t have the money when major repairs are needed.

If your operating fund is consistently short, the solution is to increase assessments, cut expenses, or both—not to raid reserves.

For a more detailed look at reserve fund accounting, including best practices for reserve studies, funding strategies, and compliance requirements, see our complete Reserve Fund Accounting Guide.

Bank reconciliation is the process of comparing your HOA’s internal accounting records to your bank statements to ensure they match.

It sounds simple, but it’s one of the most important internal controls an HOA can implement.

Without regular reconciliation, you won’t catch:

These errors don’t fix themselves. The longer they go unnoticed, the harder they are to correct.

Bank reconciliation should be done monthly, ideally by someone other than the person who writes checks or makes deposits.

If they don’t match, find the discrepancy. Don’t move forward until the accounts reconcile.

To prevent fraud and errors:

Your annual budget is the most important financial document your HOA produces.

It determines assessment amounts, guides spending decisions, and provides a benchmark for measuring financial performance throughout the year.

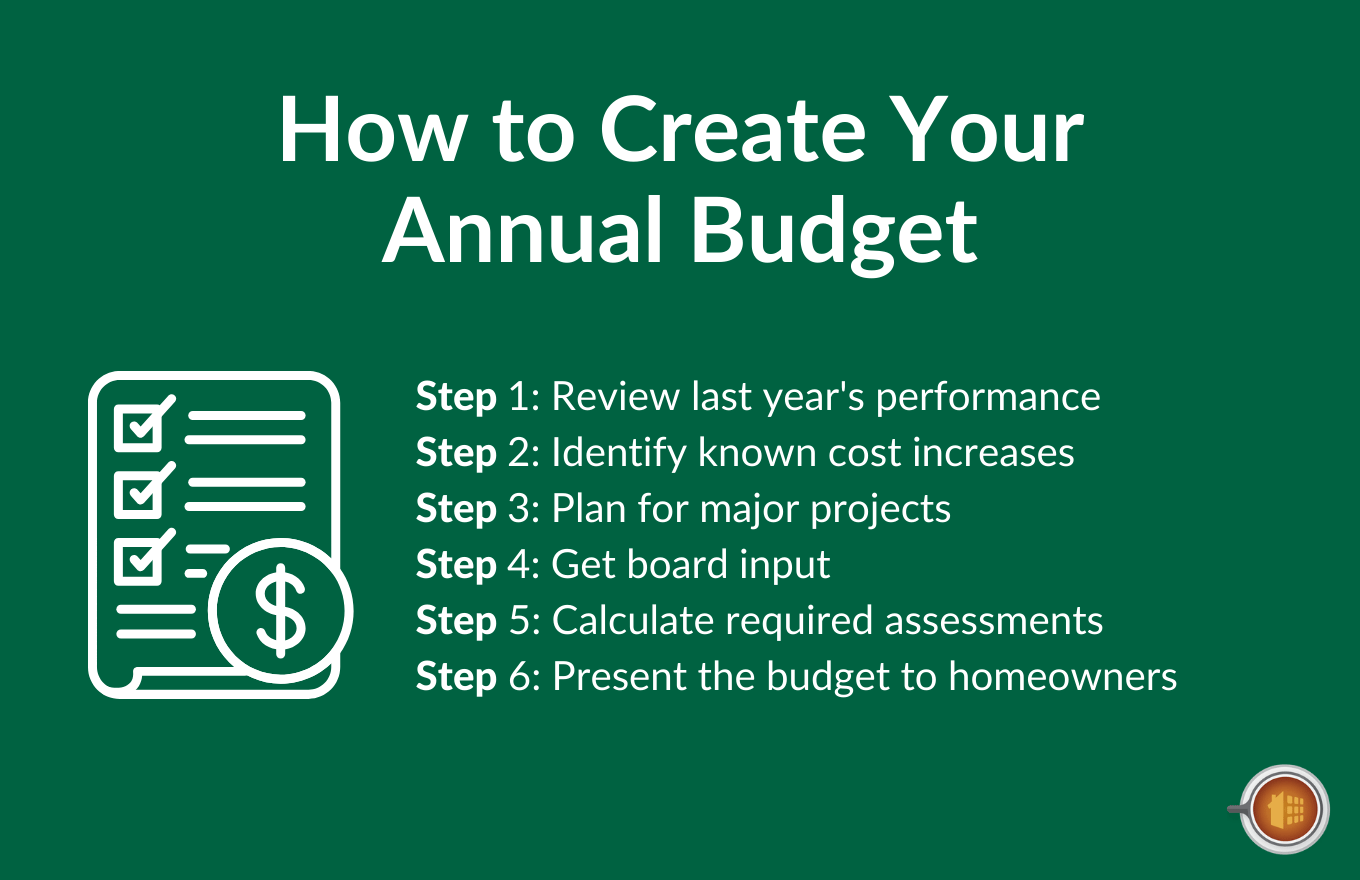

Most HOAs begin budget preparation 3-4 months before the fiscal year starts.

A lot goes into creating an annual budget, but here are the major items you’ll need to ensure you cover:

Pull up the prior year’s budget vs. actual reports. Where did you overspend? Where did you save money? Were there unexpected expenses?

Use this data to make more accurate projections for next year.

Contact your vendors and service providers to get quotes for next year. Have insurance premiums increased? Is the landscape company raising rates?

Don’t assume costs will stay flat. Budget for realistic increases.

Review your reserve study. Are any major projects scheduled for next year? Make sure reserve contributions and reserve expenditures are included in the budget.

Are there projects or improvements the board wants to tackle? New amenities? Deferred maintenance that needs attention?

These need to be budgeted for.

Once you have the total projected expenses, divide by the number of units to determine assessment amounts.

If the required assessment represents a significant increase, the board needs to decide: cut expenses, proceed with the increase, or find alternative funding sources.

Most HOAs are required to distribute the proposed budget to all homeowners before it’s finalized, often 30-60 days in advance.

This gives homeowners a chance to review and provide feedback. Some states require homeowner approval for the budget; others only require board approval.

Once your budget is approved, track actual performance against it monthly.

A budget vs. actual report shows:

This report helps you spot problems early. If you’re 3 months into the year and landscape expenses are already at 60% of the annual budget, you know you have a problem.

Budgets aren’t set in stone.

If circumstances change—a major unexpected expense, a significant cost increase, or a windfall of extra income—the board can amend the budget mid-year.

Some HOAs do formal budget revisions quarterly to keep projections realistic.

HOA board members are volunteers, often managing hundreds of thousands of dollars with minimal oversight.

Strong internal controls reduce the risk of fraud, errors, and mismanagement.

Don’t let one person control every aspect of your HOA’s finances.

The person who collects money should be different from the person who records it. The person who writes checks should be different from the person who reconciles bank accounts.

Ideal segregation of duties:

In small HOAs where this isn’t possible, have multiple board members review financial statements monthly and require dual signatures on large checks.

Require board approval for:

Document these approvals in meeting minutes.

The board should review financial statements at every meeting.

As a minimum, review:

Don’t just accept these reports without questions. If something doesn’t make sense, ask about it.

Many HOAs are required by governing documents or state law to have their finances audited or reviewed annually.

Check your governing documents and state law to see which level is required. Even if not legally required, annual reviews provide accountability and catch errors before they become serious problems.

Homeowners associations have unique tax requirements that combine elements of non-profit and business taxation.

Yes—most HOAs are subject to federal income tax.

However, HOAs have two filing options:

Under this method, the HOA functions like a regular corporation and pays tax on all income that doesn’t come from member assessments.

Investment income, rental income from facilities, and other non-member income is taxable.

Section 528 allows HOAs to file a simpler tax return and pay a flat 30% tax on certain types of income.

To qualify, at least 60% of gross income must come from member assessments, and at least 90% of expenditures must be for managing and maintaining the association.

This is usually the more favorable option for typical residential HOAs.

Missing these deadlines can result in penalties and interest charges.

Similar to your chart of accounts, taxes are complex and easy to get wrong. Here are a few costly mistakes often made the watch for:

Given the complexity of HOA taxation, most associations hire a CPA to prepare annual tax returns.

The cost is minimal compared to the risk of errors or missed deductions.

Following these best practices will keep your HOA’s finances healthy and transparent.

Spreadsheets and generic accounting software aren’t designed for HOAs.

Purpose-built HOA accounting software handles:

Good software reduces errors, saves time, and makes financial reporting easier.

Keep detailed records of all financial transactions.

Every invoice, receipt, check, deposit slip, contract—save it all. Organize records by fiscal year and keep them for at least 7 years (many states require longer retention).

Digital recordkeeping is fine, but make sure you have backups.

Financial transparency builds trust with homeowners.

Provide regular updates:

Use plain language. Not everyone understands accounting terminology, but everyone should be able to see where their assessment money is going.

Build a contingency line item into your operating budget (typically 5-10% of total expenses).

This gives you flexibility when unexpected costs arise without needing special assessments or budget amendments.

Don’t skip reserve contributions to keep assessments low.

Deferred maintenance and underfunded reserves eventually catch up with you—usually in the form of special assessments or declining property values.

Don’t automatically renew contracts year after year.

Solicit competitive bids every 3-5 years for major services (landscape, pool, management). You might find better pricing or service quality.

Money sitting in checking accounts earns almost nothing.

Move excess operating funds to high-yield savings accounts. Invest reserve funds in safe, liquid investments that earn returns while remaining accessible when needed.

Consult with a financial advisor familiar with HOA requirements before making investment decisions.

When new board members join, provide financial orientation:

Don’t assume new volunteers understand HOA finances. Invest time in training.

So far, we’ve touched on a few mistakes in creating your chart of accounts and taxes.

However, there are quite a few more HOA-specific accounting mistakes commonly made that are important to know if you’re looking to do things right.

Let’s cover them now:

Keep operating and reserve funds in separate bank accounts and track them separately in your accounting system.

Don’t “borrow” from reserves to cover operating shortfalls.

Skipping reserve contributions or contributing less than your reserve study recommends is a recipe for special assessments and deferred maintenance.

Fund reserves fully every year.

Letting delinquent accounts pile up creates cash flow problems and sends a message that paying on time doesn’t matter.

Enforce your collection policy consistently and promptly.

Skipping reconciliations means errors and discrepancies go unnoticed for months.

Reconcile every account, every month, without exception.

If actual expenses significantly exceed budget in certain categories, investigate why.

Don’t wait until year-end to discover you’re overspending.

Automatically renewing vendor contracts or hiring friends and neighbors without competitive bidding can lead to overpaying.

Get at least three quotes for any major expenditure.

Without independent verification, errors and fraud can go undetected for years.

Have your finances reviewed or audited annually, even if not legally required.

HOA board members are volunteers, and there’s a limit to how much time and expertise they can contribute.

Here’s when professional help makes sense:

A CPA can handle tax filings, annual audits, and provide guidance on accounting best practices.

Management companies typically handle assessment collection, bill payment, vendor management, financial reporting, and board support.

Purpose-built HOA accounting software streamlines financial management and provides transparency.

Mocha Manage is an HOA accounting software designed by real CPAs for community managers.

If you’re looking for an easy-to-use tool that simplifies the entire process of managing your HOA accounting, you can try it out for free (or schedule a demo for a walkthrough) by clicking here.

The right accounting approach transforms how your association operates.

You avoid special assessments. You maintain property values. You build trust with homeowners who see exactly where their money goes.

But many HOA boards struggle with spreadsheets that don’t scale, generic business software that wasn’t designed for community associations, and fragmented systems that create more work than they solve.

Mocha Manage offers a comprehensive solution built specifically for HOAs and community associations.

Purpose-built accounting tools combined with homeowner management in one integrated platform. Clean interface. Powerful features. No QuickBooks workarounds needed.

Try Mocha Manage for free to see how it can simplify your HOA’s financial management.